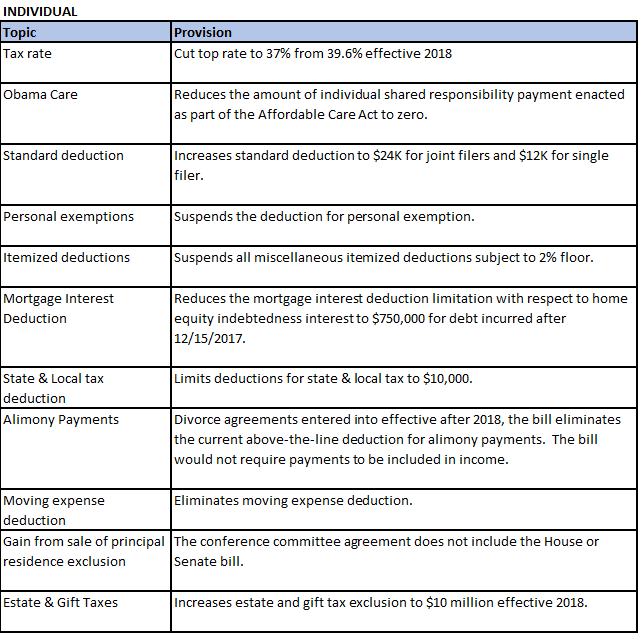

Substantial Change to Landscape of Individual Taxation

The House Ways and Means Committee unveiled its tax reform legislation and it contains many provisions that may substantially change the landscape of individual taxation, if enacted. To be signed into law, the House bill must be collaborated with the Senate bill (soon to be released), pass through both Congress of House and Senate, and signed by the president. Here are some notable provisions, generally effective for the tax year 2018, included in the House bill which may require your advance notices:

Tax Rate Change

Under the House bill, the current seven brackets would be consolidated and simplified into four brackets. The rates under the bill would be as below:

| Single Taxpayer |

|

Married Filing Jointly |

|

| Taxable income |

Tax rate |

Taxable income |

Tax rate |

| $0 to $45,000 |

12% |

$0 to $90,000 |

12% |

| $45,000 to $200,000 |

25% |

$90,000 to $260,000 |

25% |

| $200,000 to $500,000 |

35% |

$260,000 to $1,000,000 |

35% |

| $500,000 or more |

39.6% |

$1,000,000 or more |

39.6% |

Standard Deductions

Under the House bill, the standard deductions would be increased to $24,000 from $12,700 for joint filers and $12,000 from $6,350 for single individual. These amounts would be adjusted for inflation based on CPI.

Personal Exemptions

Under the provision, the deduction for personal exemptions would be repealed. Currently, the personal exemption amount is $4,050 per person (including tax filers and any dependents).

Principal Residence Gain Exclusion

Under current law, a taxpayer may exclude from gross income up to $500,000 for joint filers ($250,000 for other filers) of gain on the sale of a principal residence, if the property has been owned and used as the taxpayer’s principal residence for two out of the previous five years. However, under the House bill, the taxpayer would have to own and use a home as the taxpayer’s principal residence for five out of the previous eight years to qualify for the exclusion. In addition, the taxpayers can use the exclusion only once every five years.

Personal Deductions

The overall limitation of itemized deductions would be repealed, however, following deductions would be repealed at the same time:

- Medical expense deduction

- Casualty and theft loss deduction

- Tax preparation fee deduction

- Moving expense deduction

Alimony

Under the House bill, alimony payments would not be deductible by the payor or includible in the income of the payee. The provision would be effective for any divorce decree or separation agreement executed after 2017 and to any modification after 2017.

Mortgage Interest Deduction

The mortgage interest deduction on existing mortgages would remain the same. However, for principal residence acquired after November 2, 2017, the limit on the aggregate amount of acquisition indebtedness would be reduced to $500,000 from the current $1.1 million. Additionally, interest would be deductible only on a taxpayer’s principal residence.

State and Local Tax Deduction

Under the House bill, individuals would not be allowed an itemized deduction for state and local income or sales taxes. Additionally, real property tax deduction would be limited to $10,000.

S-corps and Partnerships (“Passthrough Entity”)

Passive activity income from a passthrough entity would be taxed at the 25% tax rate. Generally, nonpassvie activity income from a passthrough entity would be taxed at ordinary income rate. This provision is expected to give a large tax break for real estate investors (including Donald Trump himself).

1031 Like-Kind Exchange Applies to Real Estate Only

The bill limits tax deferral provision under Section 1031 (known as “Like-Kind Exchange”) to real estate. Currently, business owners were able to defer taxation on gain disposing a business by investing in a similar business. However, this tax deferral provision would be allowed for real estate transactions.

Some of these provisions contained in the House bill would have a direct impact to many of us. Although we are expecting mark-ups by the Senate in the coming weeks before the bill gets enacted, however ones should continually monitor the legislation development specially if you are contemplating a transaction.